1. Introduction

Under the continued implementation of the Rectangular Strategy Phase IV, the Royal Government of Cambodia has prioritized the modernization of legal and institutional frameworks to promote private sector growth and attract foreign direct investment, particularly in capital-intensive sectors such as real estate, infrastructure, and tourism. While this strategy has stimulated foreign investor interest, land-based investment remains constrained by Article 44 of the Cambodian Constitution, which limits land ownership to individuals and legal entities holding Cambodian nationality. In response, some investors have adopted indirect structures such as long-term leases, nominee arrangements and land-holding companies to gain control without formal title over the land. However, these arrangements lack formal legal recognition under Cambodian law and remain vulnerable to enforcement uncertainty, regulatory scrutiny, and compliance risks.

In response to the structural challenges outlined above, the Royal Government enacted the Law on Trusts, Royal Kram No. NS/RKM/0119/002, dated 2 January 2019, to establish a formal and regulated framework for trust arrangements within the Kingdom of Cambodia. This structure separates legal title from beneficial ownership, enabling foreigners to hold a beneficial interest in property in Cambodia through a Cambodian trustee, as a legally recognized mechanism to overcome the constitutional restrictions on land ownership imposed on foreigners. Implementation of the trust regime is further supported by several regulations issued under the authority of the Trust Regulator (“TR”), aimed at enhancing procedures, licensing, and operational oversight within the trust sector. Most recently, Prakas No. 192 dated 12 March 2025, issued by the Ministry of Economy and Finance, outlines the tax rules and procedures applicable to trust arrangements.

This article outlines the legal and tax implications that form the foundation of Cambodia’s trust framework, with a particular focus on its application in real estate investment. Drawing on practical scenarios, the analysis addresses key tax issues arising in both domestic trust arrangements and critically examines whether the trust mechanism, as currently regulated, effectively supports the policy objective of attracting foreign investors to Cambodia’s real estate sector.

2. Overview of Legal and Tax Framework

Trusts are often promoted as a more structured and potentially tax-efficient mechanism for managing property, including real estate. Under trust laws and regulations, several types of trusts are recognized, including commercial trusts, individual trusts, social trusts, and public trusts. For the purpose of this article, we will primarily focus on commercial trust and individual trust, as they are more relevant in the context of private investment and asset structuring in Cambodia. In practice, trust arrangements generally involve three key stages, each with distinct legal, operational, and tax considerations: (i) the establishment of the trust, (ii) the ongoing management and operation of the trust, and (iii) the termination or dissolution of the trust. Each of these stages carries its own set of tax implications, which must be carefully assessed to ensure full compliance and to optimize tax efficiency throughout the trust’s lifecycle. For a more detailed discussion, please refer to Section 3.

Under the Law on Trusts and regulations, a trust is established when a settlor (or trustor) transfers property or funds to a licensed trustee recognized by the TR—who may be either an individual or a trust company—to manage for the sole benefit of the beneficiaries, pursuant to a formal trust deed that clearly sets out the trust’s purpose, the duties and powers of the trustee, and the identity of the beneficiaries. The trust becomes legally enforceable and valid upon the effective transfer of property to the licensed trustee and the registration of the trust with the TR within 3 (three) months from the date of its establishment.

Once the trust is registered with the TR, the trustee assumes legal responsibility for managing the trust property in accordance with the trust deed and regulatory obligations. Trust property is protected from the trustee’s personal liabilities, and any material changes such as asset transfers, trustee replacements, or investments require TR’s approval according to Article 22 of Law on Trusts. Trusts are subject to ongoing regulatory supervision, particularly in cases of non-compliance or misuse of assets. Termination of trust may occur upon fulfillment of the trust’s purpose, expiry, court order, or settlor decision, with prior notice to and approval from the TR, and distribution of assets as provided in the trust deed and applicable laws, as provided under Article 32 of the Law on Trusts.

Under the Cambodian trust regime, various taxes may apply depending on the nature of the trust structure and the transactions involved throughout its lifecycle. These may include stamp tax, capital gains tax, withholding tax, tax on property rental, property tax, and unused land tax.

3. Each Structure and Key Tax Issues in connection with Trust Arrangement

Prakas No. 192 on Tax Rules and Procedures for Trust primarily sets out general definitions of key terms relevant to trust arrangements, along with high-level provisions on the applicable tax implications, illustrated by some basic examples. While informative, the Prakas may not comprehensively address all concerns typically raised by prospective investors in the Cambodian real estate market. For a general overview of Prakas No. 192, please refer to our Newsletter No. 129.

In this article, by contrast, we seek to examine the tax implications of trust arrangements based on the three key stages identified, namely: (i) the establishment of the trust, (ii) the ongoing management and operation of the trust, and (iii) the termination or dissolution of the trust. Each transition from one stage to the next may give rise to distinct tax consequences under applicable laws and regulations.

The following section sets out a detailed overview of common transactions occurred throughout the lifecycle of a trust, accompanied by scenario-based analyses to illustrate the practical application of the relevant rules as they pertain to settlors, trustees, and beneficiaries. These illustrations are intended to enhance understanding of the tax compliance obligations provided in the new Prakas No. 192.

3.1. Establishment of Trust

The establishment phase is the foundation of a valid trust arrangement. It involves the legal creation of the trust through the execution of a trust deed, registration with the TR, and the initial transfer of property or funds from the settlor to the trustee. The trust deed defines the purpose of the trust, the roles and responsibilities of the parties (settlor, trustee, and beneficiaries), and the rules for property administration and management.

Article 8 (3) of Prakas No. 192 broadly provides that “in case there is a transfer of ownership, right of possession, or contribution of shares involving immovable and movable property, trust property, or a transfer of shares, such transactions shall fall within the scope of the stamp tax.” This wording seems to suggest that transfers occurring within the framework of a trust arrangement could fall within the scope of stamp tax. However, while the establishment of a trust typically involves the transfer of an asset to the trustee, such transfer does not necessarily give rise to an immediate tax liability. The tax implications may vary depending on the nature of the asset transferred, the structure of the trust arrangement, and the legal characterization of the transaction under tax law. In certain circumstances, there may still be rooms to argue that the transfer should not be subject to tax.

Below are 3 (three) common scenarios illustrating the legal and tax implications that may arise during the establishment phase, whether it is taxable or non-taxable events:

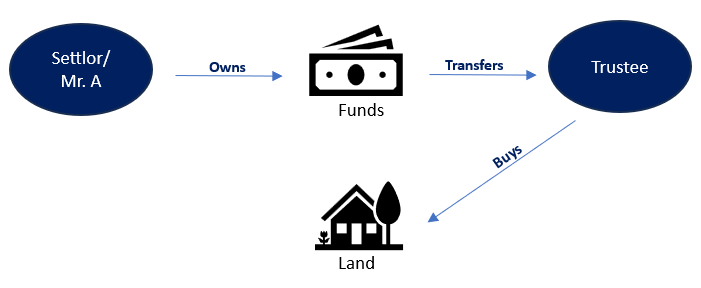

Scenario 1: Transfer of Funds to the Trustee for the Purpose of Acquiring Property

A foreign investor, Mr. A, contributes USD 750,000 to a trust account managed by a licensed trustee. The trustee is instructed to use the funds to purchase a plot of land in Phnom Penh on behalf of Mr. A.

- The initial transfer of funds to the trustee is generally regarded as a non-taxable transaction, provided that the funds are intended for the acquisition of immovable property on behalf of the settlor. Based on Article 7 of Prakas No. 192, this treatment applies on the condition that the trust is duly registered with the TR, and the transaction is clearly documented within the trust deed and supported by formal financial records.

However, the subsequent acquisition of immovable property by the trustee may give rise to a stamp tax liability at the rate of 4%, applicable upon the execution of a sale and purchase agreement for the transfer of legal title. This tax implication is imposed in accordance with tax laws and regulations. The trustee, as the legal transferee of the property, bears the responsibility for ensuring proper valuation, declaration, and payment of this tax at the time of registration. This scenario can be found in examples 2 and 4 of Prakas No. 192. Conversely, if the trustee is instructed to acquire a house or condominium from licensed property developers, the available tax incentives may apply in this regard according to Article 10 of Prakas No. 192.

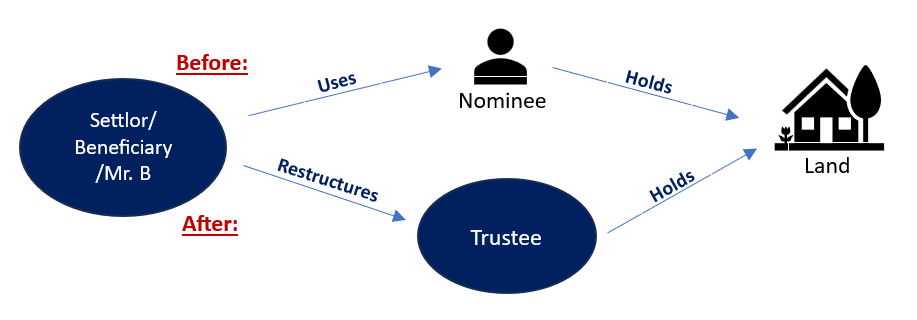

Scenario 2: Restructuring from Nominee Arrangement to Trustee

Mr. B, a foreign investor, has previously maintained an interest in land in Cambodia under a nominee arrangement, whereby legal title was registered in the name of a Cambodian national. In light of growing regulatory scrutiny and the risks associated with the informal ownership structures, Mr. B dissolves the nominee arrangement and restructures the ownership of the property into a formally registered trust, managed by a licensed trustee.

- While this restructuring reflects a transition from an informal nominee arrangement to a legally compliant trust structure, it entails a formal transfer of legal title from the nominee to the trustee. Pursuant to Article 8 (3) of Prakas No. 192, as referenced above, such a transfer may be construed as a transfer of ownership, which would fall within the scope of the stamp tax and, accordingly, be subject to tax at the rate of 4% given that Prakas No. 192 is silent on the specific treatment on restructuring transactions. Therefore, no automatic exemption from stamp tax can be assumed under the current legal framework.

Despite the current wording of the applicable provisions, there is a compelling argument that such a transaction should not be subject to 4% stamp tax, given that the beneficial ownership remains unchanged and the restructuring is undertaken solely to bring the arrangement into compliance with existing laws and regulations. Rather than constituting a commercial transaction, the transfer should be viewed as the formalization of an existing legal arrangement —the very type of situation that the trust regime is intended to regularize. No consideration is received, and no income or gain is realized from such restructuring.

Moreover, if such formalization were to be deferred to a later date, there may be adverse tax implications from a capital gains tax perspective, depending on the appreciation in asset value and the prevailing tax regime at the time of transfer. This could render the restructuring financially unviable and act as a disincentive to legal compliance.

However, it has been reported that the private sector has recently submitted a formal request to the tax administration seeking reconsideration of the application of the 4% stamp tax to the transfer of immovable property from personal ownership into a corporate entity wholly owned by the original landowner, in the context of corporate restructuring and business expansion. The submission is based on the view that the imposition of such tax could undermine the economic viability of such transactions and hinder growth within the corporate framework. The tax administration should be currently reviewing this matter taking into account the non-commercial nature of the transfer and its underlying purpose of restructuring and formalizing existing ownership arrangements. The final position has not yet been formally adopted.

Should such a precedent be established, it may provide persuasive grounds for similar treatment in the trust context, particularly for asset transfers undertaken purely for restructuring and compliance purposes, as opposed to transactions motivated by commercial gain.

3.2. Operational Management of Trust

Once a trust is validly established and duly registered, the settlor transfers legal ownership of designated assets such as cash, securities, or immovable property to the trustee, who then assumes full legal title and manages these assets in a fiduciary capacity, strictly in accordance with the trust deed and for the benefit of the designated beneficiaries. The trustee’s responsibilities include the administration, safeguarding, and potential disposal of trust property.

The trustee also bears primary responsibility for the management and filing of all tax obligations related to trust property, including real estate pursuant to Article 9 of Prakas No. 192. This provision is of primary importance, as it emphasizes the need for trustees to possess a professional understanding of applicable tax laws, especially given the complexity and regularity of monthly, annual or even transactional tax compliance. This may also include property-related taxes. As stipulated in Article 153, and Article 173 of the Law on Taxation, the trustee acts as the legal owner may be responsible for filing and remitting property-related taxes, namely property tax or unused land tax (if applicable).

This raises important questions regarding the allocation of liability in the event of a tax audit. While any underpaid tax is legally the obligation of the trust account itself, the trustee is the party required to file tax returns on behalf of the trust. A plain reading of Article 9 suggests that the trustee acts in the capacity of a tax agent, with a filing obligation rather than personal liability for the trust’s tax obligations.

However, from a legal perspective, there may still be grounds for recourse against the trustee by the settlor or beneficiaries in the event of a professional error or negligence in the performance of the trustee’s tax-related duties. As such, trustees must exercise a high degree of diligence to mitigate potential exposure.

Overall, the trustee must also ensure broader tax compliance under the trust arrangement, including the following duties:

-

- maintain accurate accounting records for all trust activities;

- file monthly and annual tax returns to the tax administration;

- remit applicable taxes to tax administration.

The following are 3 (three) common scenarios that arise during the operational management of a trust:

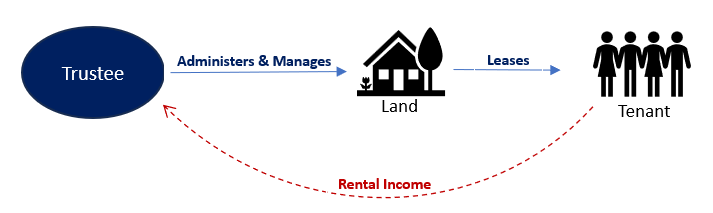

Scenario 3: Rental Income from Trust Property

The trustee, acting on behalf of a registered trust established by the settlor, leases a commercial property (i.e. land) located in Phnom Penh to tenants. The property forms part of the trust’s asset portfolio and is managed and maintained by the trustee in accordance with the trust deed. The leasing activity generates rental income.

- Under Prakas No. 192, a trust is treated as a separate taxable transaction. Therefore, income derived from leasing trust property is subject to tax on property rental, which will be declared and paid to the tax administration by the trustee.

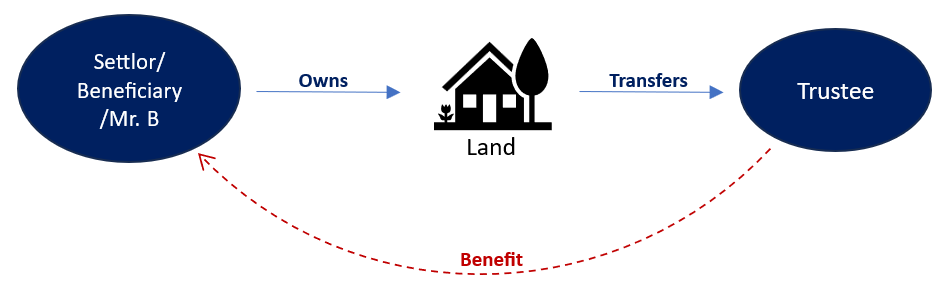

Scenario 4: Settlor as the Beneficiary Using Property after Transferring Property to Trustee

Mr. B transfers the legal title of a plot of land to a licensed trustee. The trust is established for long-term property management and future distribution to designated beneficiaries. However, instead of leasing the property, Mr. B, who is also designated as a beneficiary retains, personal use of the land for residential or commercial purposes without paying rent.

- Based on Article 8 (3) of Prakas No. 192, any transfer of ownership, right of possession, or contribution of shares involving immovable or movable property, trust property, or shares is considered a taxable event and is subject to stamp tax at the rate of 4%. In the context of Scenario 4, the transfer of the legal title of immovable property to a trustee by Mr. B may fall within the scope of stamp tax. Furthermore, if such a transfer takes place in the future, there could also be tax implications from a capital gains tax standpoint. As mentioned above, the transaction where no cash is received should also be tax-neutral or at least of minimal tax implication given that the trustee is acting solely as a conduit for the purpose of holding the property on behalf of the settlor and/or beneficiary(s).

Based on a textual reading of Articles 7 and 8 of Prakas No. 192, it appears to suggest that where trust property is utilized or made available for use, there should generally be consideration or income arising from such use. This implies a presumption that the trust property, when put to use, should generate revenue.

However, where the settlor and the beneficiary are the same person (i.e., there is no change in beneficial ownership), and the trust deed expressly authorizes such person to use and enjoy the trust property (e.g., land), it raises the question of whether any consideration should be deemed necessary in such a case. In our view, where the settlor-beneficiary is exercising rights already conferred under the trust deed, and there is no transfer of benefit to a third party, such use should not, in principle, trigger a taxable event.

Nonetheless, given the absence of express guidance on this point in Prakas No. 192, we recommend that formal clarification be sought from the tax administration to ensure legal certainty and mitigate any potential tax exposure.

Scenario 5: Sale of Property Held by Trust

A licensed trustee, acting on behalf of a registered trust, sells a plot of land—held in trust—to a new buyer, Ms. X. The land was originally acquired using funds contributed by the settlor and was managed by the trustee as a long-term investment in accordance with the trust deed. Upon sale, the transaction results in realized capital gains.

- In accordance with Prakas No. 192 and relevant provisions of the Law on Taxation, the sale of land by a trustee is a taxable event and may be subject to the following tax obligations:

- Capital Gains Tax: the gains realized from the sale of immovable property are subject to capital gains tax at a rate of 20% (if applicable). The taxable gain is calculated based on (i) the difference between the selling price and the acquisition cost, adjusted for any allowable expenses, including improvement costs and depreciation (if applicable) or (ii) on the lump sum deduction of 80% of the sale price.

-

- Stamp Tax: the transfer of legal ownership of land is subject to the 4% stamp tax in the hand of the buyer.

-

- Value Added Tax (VAT): Articles 7 and 8 of Prakas No. 192 do not expressly impose a VAT obligation on the disposal of trust property. Under the prevailing tax framework, the sale of land is generally exempt from VAT; however, ancillary elements—such as buildings or other VATable items—may give rise to VAT liabilities. This raises a point of interpretation as to whether, in the event of a disposal of VATable trust assets, the trustee is required to collect and remit VAT in its own capacity as a registered taxpayer, or whether the trustee merely acts in a representative capacity and applies the tax treatment applicable to the underlying trust property.

In our view, the latter interpretation appears more consistent with the overall intent of Prakas No. 192. For instance, while Article 4 outlines the various forms of trusts recognized under the Prakas, Article 2 specifies that “the provisions apply to settlors, trustees, and beneficiaries whether resident or non-resident who are engaged in activities related to trusts established in the Kingdom of Cambodia, excluding trusts that take the form of a company or enterprise”. This wording suggests that the Prakas is intended to apply primarily to individuals and not to treat trust accounts as self-assessment taxpayers for VAT purposes. Furthermore, the absence of any reference to VAT in Articles 7 and 8 supports the view that VAT obligations are not directly imposed under the current scope of Prakas No. 192. That said, due to the lack of explicit guidance, and in the interest of certainty and compliance, seeking a confirmation from the tax administration on the applicable VAT treatment in respect of the disposal of trust assets would be recommended.

3.3. Termination of Trust

The termination of a trust marks the final stage of its legal and operational lifecycle. This phase involves the orderly winding down of the trust assets, which may include changes to the trust structure such as the replacement of a trustee and the substitution of beneficiaries. Termination must be executed strictly in accordance with the terms of the trust deed and relevant provisions of laws and regulations.

The following are 2 (two) common issues that often arise during the final stage of a trust’s lifecycle:

Scenario 6: Change of Trustee

Due to internal policy changes and succession planning of the trustee, the settlor appoints a new licensed trustee to replace the existing one. As part of this process, the trust property including immovable property and financial assets is formally transferred from the outgoing trustee to the newly appointed trustee. The trust’s structure, beneficiaries, and underlying purpose remain unchanged.

- Where a trustee is replaced, the transfer of legal title to trust property from the outgoing trustee to the newly appointed trustee should, in principle, not constitute a taxable event, provided that there is no change in the beneficial ownership and the transaction occurs within the same trust structure.

However, due to the absence of specific guidance under Prakas No. 192, there remains a risk that the transfer may be subject to the 4% stamp tax and potentially capital gains tax, depending on the timing and interpretation of the transaction. A literal application of the Prakas could give rise to such tax exposure, notwithstanding the non-commercial nature of the transfer and the continuity of the trust arrangement.

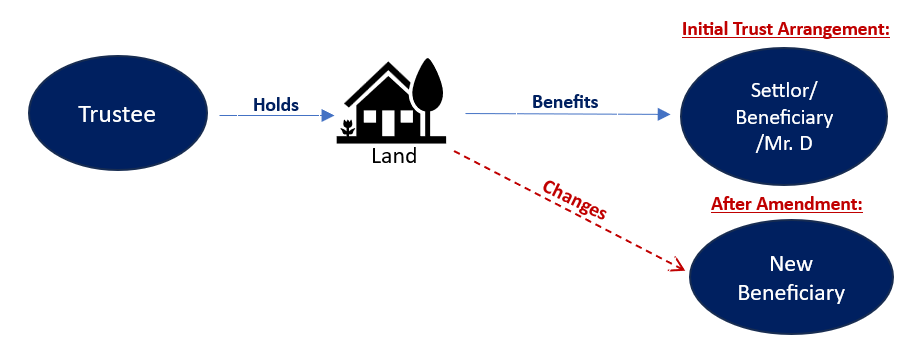

Scenario 7: Change of Beneficiaries

Mr. D, the settlor of a registered trust, decides to revise the trust arrangement to replace one of the existing beneficiaries with another individual for personal succession planning reasons. The trustee, in accordance with the terms of the trust deed, executes an amendment reflecting the change in the list of beneficiaries. No distribution of assets is made at the time of the amendment.

- Provided that no assets are distributed and no new economic rights are conferred immediately upon amendment, a change of beneficiaries is generally not regarded as a taxable event under laws and regulations.

However, the tax administration may take the view that a change in beneficiaries could give rise to tax implications if such change results in any form of consideration being provided to the settlor or existing beneficiaries. In such circumstances, the transaction may be treated as a transfer of beneficial ownership, thereby triggering potential tax liabilities, i.e, from stamp tax and capital gains tax standpoints.

4. Conclusion

Trust arrangements present a powerful tool for managing and investing in real estate in Cambodia. When structured correctly, they offer enhanced legal certainty, improved asset protection, and potentially favorable tax treatment compared to traditional holding structures.

The current trust framework anchored in the Law on Trusts and supported by implementing regulations such as Prakas No. 192 has made commendable progress in laying the groundwork for regulated fiduciary arrangements. It provides legal recognition for the separation of legal title and beneficial interest, defines the roles of key parties, and outlines general tax obligations applicable at each phase of the trust’s lifecycle.

However, in our view, the legal framework remains in an early phase of implementation, and the practical application still presents several uncertainties, particularly around tax treatment in restructuring scenarios, such as settlor-beneficiary arrangements. The absence of detailed regulatory guidance in these areas can expose investors and trustees to compliance risks.

To strengthen investor confidence and enhance the effectiveness of the trust regime, further guidance, especially from a tax standpoint needs to be issued. Doing so will not only close existing regulatory gaps but also promote a more transparent, predictable, and investor-friendly environment.

In conclusion, Cambodia’s trust regime holds strong potential to serve as a cornerstone of foreign real estate investment and long-term asset structuring. But to fully realize that potential, it requires continued legal development, tax clarity, and institutional support. Investors and practitioners are strongly advised to assess each trust arrangement on a case-by-case basis and seek professional advice to ensure alignment with both legal requirements and tax expectations.

In our next article, we will explore the complexities of trust arrangements from a cross-border perspective, focusing on scenarios involving settlors and/or beneficiaries who are tax residents of jurisdictions with, or without, a double taxation agreement (DTA) with Cambodia. The analysis will also address the potential implications arising from the OECD’s Base Erosion and Profit Shifting (BEPS) initiatives, including both BEPS 1.0 and BEPS 2.0.

Important Notice: The information contained in this article is provided for general informational purposes only and does not constitute legal advice. It has been prepared by the legal and tax team at Davies SM Attorneys-at-Law, based on Cambodian laws and regulations publicly available as of 22 April 2025. For legal advice customized to your specific circumstances, please contact our Principal Lawyer, Ms. Pheng Sovicheany.

This tax update is brought to you by Davies SM Attorneys-at-law.