Cambodia’s bilateral trade with Singapore surged 191.5% year-on-year in January–February 2026, according to data from the General Department of Customs and Excise (GDCE), reported in the Khmer Times on 26 March 2026. The headline figure is striking, but its composition – and its context – tells a more important story for businesses and investors seeking to understand what is structurally shifting in Cambodia’s trade geography.

The surge was driven almost entirely by a spike in Cambodian imports from Singapore, which soared 209.3% to USD 322 million over the two-month period. Cambodia’s exports to Singapore, by contrast, grew a modest 18%, totaling USD 12.68 million. The resulting trade imbalance of approximately USD 309 million for just two months underscores a structural asymmetry that has characterized this bilateral relationship for some time.

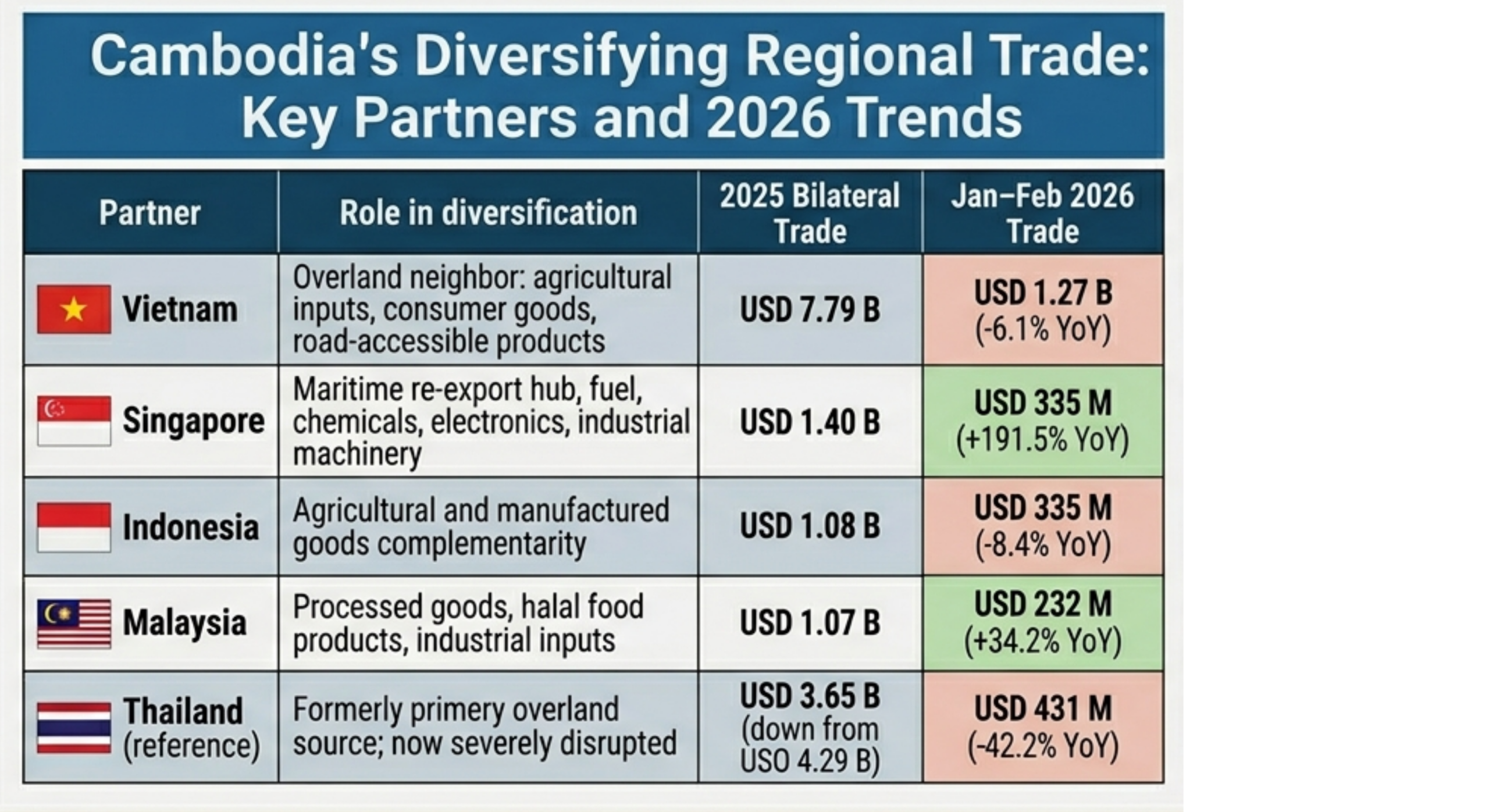

Setting the Scene: Cambodia’s Trade in 2025

Cambodia’s total international trade exceeded USD 64 billion in 2025, a 16.8% increase year-on-year, with exports reaching USD 30.14 billion and imports USD 33.88 billion. Deputy Prime Minister Sun Chanthol described the near-parity between exports and imports as a historic milestone – a marked departure from Cambodia’s earlier pattern of import-heavy trade. China remained the largest trading partner at over USD 19 billion, followed by the United States at over USD 13 billion and Vietnam at more than USD 7.7 billion. Singapore’s full-year 2025 bilateral trade stood at approximately USD 1.4 billion — context that makes the early 2026 trajectory all the more significant.

A Corridor-wide Shift: the Thai Border Effect

The border conflict between Cambodia and Thailand that escalated through the second half of 2025 disrupted Cambodia’s most significant overland import corridor. Bilateral trade with Thailand contracted around 15% in 2025 to USD 3.7 billion from USD 4.3 billion in 2024, and by October 2025, cross-border trade had fallen by approximately 99% due to border restrictions. With the situation yet to be resolved, the import rerouting that began in 2025 has carried into 2026.

In response, Cambodian importers diversified sourcing across multiple ASEAN partners – each absorbing different portions of redirected demand through different trade channels, as summarized below.

Singapore’s role in this picture is distinct from that of its mainland ASEAN neighbors. Where Vietnam and Malaysia absorbed more of the consumer and agricultural commodity flows previously supplied overland from Thailand, Singapore captured a different and higher-value segment of the import basket – fuel, chemicals, electronics, and industrial machinery routed through its maritime logistics infrastructure. A structural caveat also applies: goods originating in third countries are frequently recorded as Singapore-origin imports upon re-export, an effect that is particularly pronounced in fuel and petroleum flows and that amplifies the bilateral headline figure.

Beyond the import rerouting, analysts suggest that Cambodian businesses may also have front-loaded procurement in early 2026 ahead of anticipated growth in domestic consumption and infrastructure spending – adding further momentum to an already elevated baseline.

An Important Caveat on Timing

These figures cover January–February 2026 – before the outbreak of the US-Israel-Iran conflict on 28 February 2026, which has since triggered significant disruptions to global oil and gas markets, shipping costs, and regional supply chains. Given that fuel and petroleum products constitute a significant component of Cambodia’s Singapore imports, the downstream effects of the conflict on this corridor will be important to monitor. If energy prices remain elevated and freight costs rise, the import bill through Singapore could increase further even without a corresponding rise in volumes, widening the bilateral deficit.

The Export Gap — and the Opportunity

While officials have flagged the need to expand Cambodia’s outbound shipments, the conversation around Cambodian exports tends to default to the familiar trio of garments, footwear, and travel goods. This understates the breadth of what Cambodia actually produces and exports – and the opportunity that remains underexploited in the Singapore–Cambodia corridor specifically.

Cambodia is, perhaps surprisingly to many international businesses and investors, among the world’s top five exporters of bicycles – and the world’s second largest exporter of Christmas tree lighting after China. Furniture, processed agricultural products, finished food items, wiring harnesses, electronic components, and a growing range of light manufactured goods form part of the export basket. These are not marginal categories – they represent sectors where Cambodia has genuine and growing competitive presence, underpinned by preferential market access under RCEP, the Everything-but-Arms (EBA) tariff exemption for exports to the EU market, bilateral FTAs, and the government’s industrial diversification agenda. Yet they remain less visible internationally and are underrepresented in bilateral Singapore–Cambodia trade flows relative to their potential.

The same supply chain reconfiguration that has increased Cambodia’s import dependence on maritime ASEAN partners also opens a mirror-image question: which of those same partners – Singapore-based traders, distributors, F&B importers, retailers, and procurement networks – could be doing more to bring Cambodian-manufactured goods to regional and global markets? Investment into Cambodia’s agro-processing, food manufacturing, and light industrial sectors – priority areas supported by government policy, Khmer Enterprise’s entrepreneurial ecosystem, and Cambodia’s expanding network of preferential trade arrangements – can directly address the supply-side constraints that keep export volumes modest. Strengthening export capacity is not only a commercial opportunity; it is, as Cambodian trade officials have noted, the key lever for narrowing what is becoming a structurally wide bilateral deficit with Singapore.

The Broader Picture

Cambodia’s total trade reached USD 11.11 billion in the first two months of 2026, up 17.6% year-on-year, building on a full-year 2025 total that exceeded USD 64 billion and brought exports and imports to near-parity for the first time. The Kingdom’s deeper integration into ASEAN supply chains – reinforced by RCEP, bilateral FTAs, and EBA – creates a structurally more resilient trade base, one that the import diversification of the past year has further strengthened.

Translating that into a more balanced, two-way relationship with Singapore – and with ASEAN partners more broadly – will require deliberate effort: on export promotion, product awareness, market access, and the business matching that connects Cambodian producers to regional trading and distribution networks. The bilateral data tells us the corridor is active and growing. What it does not yet reflect is the full range of what Cambodia has to offer as an exporter.

These are the conversations that matter for businesses and investors seeking to move beyond the headline numbers – and to position themselves ahead of the curve in one of Southeast Asia’s most dynamic and underappreciated markets.

Source: Cambodia’s trade with Singapore surges over 190% | Khmer Times (khmertimeskh.com)